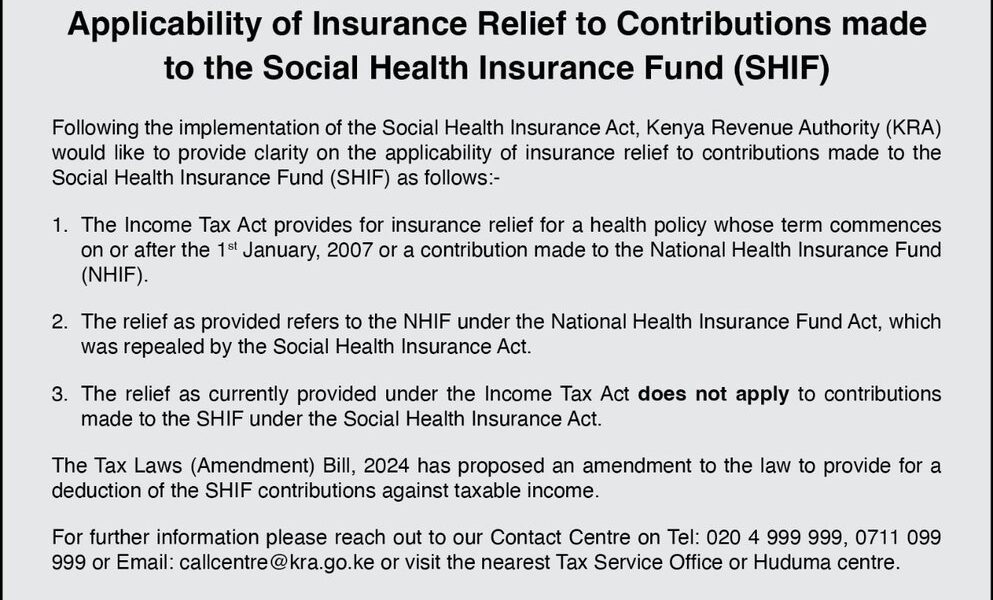

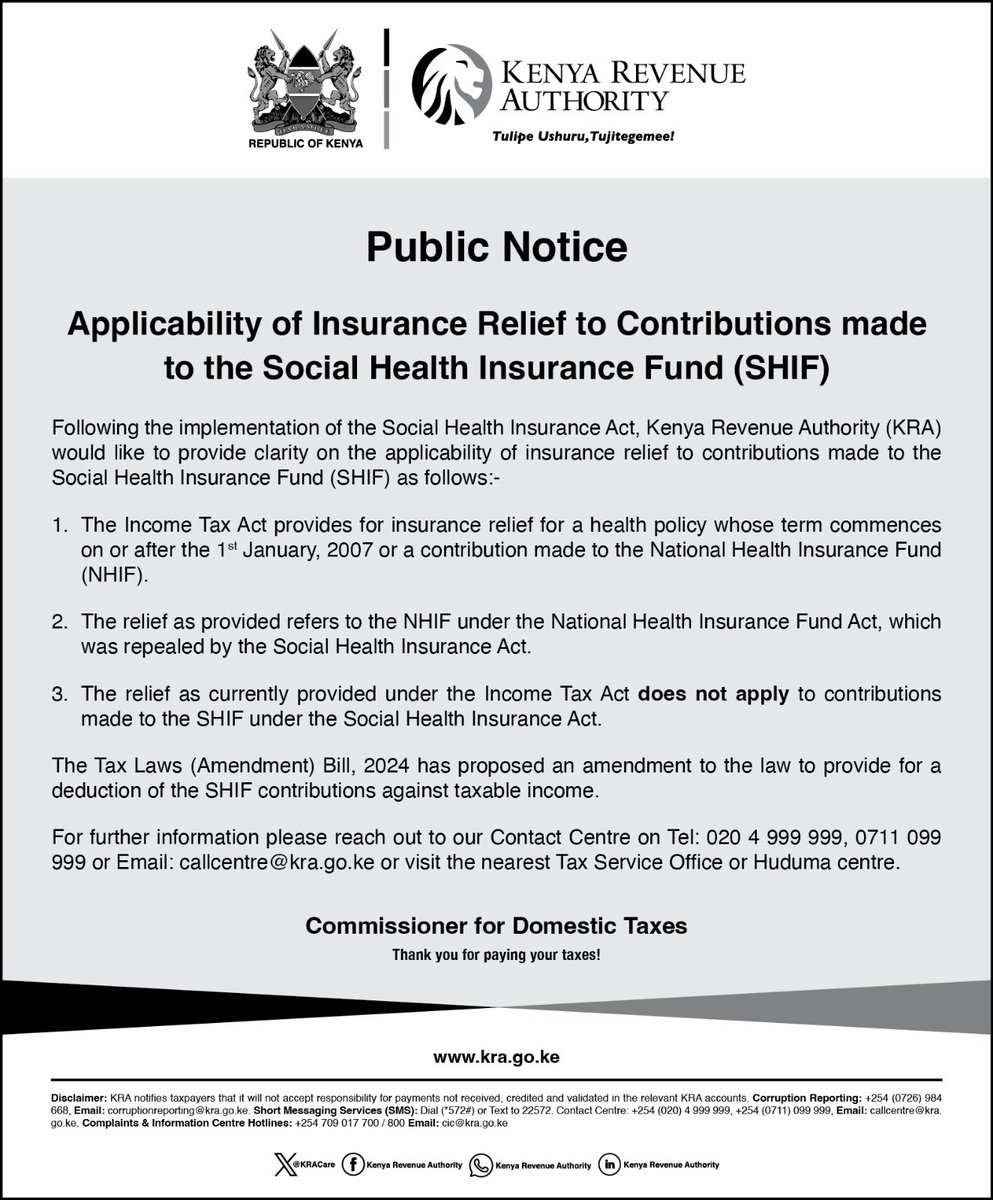

The Kenya Revenue Authority (KRA) recently issued a public notice clarifying the applicability of insurance relief on contributions made to the Social Health Insurance Fund (SHIF). This notice comes after the implementation of the Social Health Insurance Act, which replaced the National Health Insurance Fund (NHIF) with SHIF, sparking widespread discussions on the tax implications for contributors.

Key Points from KRA’s Notice

- Current Tax Relief Law

The Income Tax Act provides insurance relief for health policies beginning on or after January 1, 2007, or for contributions made to NHIF. This has been the case for years, where NHIF contributions were eligible for relief, making them deductible against taxable income. This policy was particularly beneficial for low- and middle-income earners who rely on NHIF for affordable healthcare coverage. - NHIF Replaced by SHIF

With the enactment of the Social Health Insurance Act, NHIF was repealed and replaced by SHIF. This legislative change raised questions about the tax benefits previously associated with NHIF contributions. KRA’s notice clearly states that the insurance relief provided under the Income Tax Act was meant solely for NHIF contributions as specified by the National Health Insurance Fund Act, which is no longer in effect. - SHIF Contributions Ineligible for Current Insurance Relief

KRA clarified that, as it stands, contributions to SHIF are not eligible for insurance relief under the current Income Tax Act. This means that individuals contributing to SHIF will not receive the same tax deductions that were previously available under NHIF, potentially impacting take-home pay for some workers. - Proposed Tax Law Changes

The notice also highlights the ongoing review of the Tax Laws (Amendment) Bill, 2024. This bill includes a proposal to amend the law to allow for SHIF contributions to be deducted against taxable income. If this bill passes, contributors to SHIF could once again benefit from tax deductions similar to those previously associated with NHIF. However, until this amendment is enacted, SHIF contributions will not qualify for insurance relief.

Public Reactions and Concerns

Many Kenyans have expressed concerns over the immediate impact of these clarifications, particularly those who relied on NHIF relief to reduce their tax liabilities. The shift to SHIF without immediate relief has left some contributors feeling the pinch in their budgets. Public discussions on social media reveal a general call for quick action on the proposed amendments to avoid financial strain on families already grappling with economic challenges.

What This Means for You

For individuals currently contributing to SHIF, it’s essential to be aware that your contributions do not qualify for tax relief under the present regulations. To mitigate any financial surprises, consider consulting a tax advisor or reaching out to KRA’s support services for further guidance on how this policy change might affect your tax planning.

For further details or queries, KRA encourages Kenyans to reach out through their Contact Centre by dialing 020 4 999 999, 0711 099 999, or by emailing callcentre@kra.go.ke.

Possible Future Developments

The Tax Laws (Amendment) Bill, 2024, if passed, will allow for SHIF contributions to be deducted from taxable income, reinstating the relief that NHIF contributions once provided. Until this bill is approved, taxpayers will need to adjust to the current reality.